The Rise of Multi Retirements: A Quality of Life special report[@a-quality-of-life-special-report]

The report highlights the emerging trend of flexible retirement, following a survey of over 10,000 affluent individuals across 12 global markets.

Retirement isn’t just a life stage. It’s a lifestyle.

By Jenny Wang

Head of Premier Wealth Solutions, International Wealth and Premier Banking, HSBC

Key takeaways

- Retirement is reimagined today – Affluent investors are considering non-linear retirement and taking more fluid, frequent and intentional pauses across their lifetime.

- Tension between short-term aspirations and long-term goals – While 5 in 10 affluent investors have intention to take mini retirement in the future, more than 30% indicate that they plan to draw from pension plans or retirement accounts to fund their mini retirement, a sign that they will need more savings for their final retirement.

- Ensuring financial security for mini retirement and the long haul – 5 steps to empower affluent investors to withstand inflation and create a personalised financial plan.

Affluent investors are no longer waiting until later life to take their retirement, with some now reimagining more fluid, frequent and intentional pauses in their careers.

The traditional approach to retirement planning – study, work, then retire – is being passed over by 5 in 10 affluent investors according to our new research.

Nearly half (49%) of those surveyed who are considering a mini retirement are planning to take between two and three breaks across their lifetime. They view the optimal length of a mini retirement to be between 6 and 12 months, with 47 the ideal age for taking the first pause.

So, what is a mini retirement? They can be defined as a clean career break, typically lasting 6-12 months, for individuals to travel, spend quality time with family, pursue hobbies, or develop new skills. These intentional pauses differ from a sabbatical as they’re typically last longer and can lead to significant life changes such as a new career path or starting a business[@intentional-pauses].

The report also highlights a shift in priorities among affluent investors as they look to improve their quality of life, focusing on personal fulfilment and well-being.[@a-quality-of-life-special-report] They are redefining what wealth and success mean to them, measuring in time and well-being rather than traditional financial milestones such as accumulation of assets or a larger bank balance. Nearly three quarters (74%) of those surveyed consider mini retirements as a route to enhance their overall quality of life.

Of those intending to take a mini retirement, there was remarkable consistency across the generations in terms of the number of these breaks they plan to take across their lives. Gen Z and Millennials plan for an average of three mini retirements, while Gen X and Baby Boomers report the intention to take an average of 2.9 and 2.8 breaks, respectively.

Motivations for a mini retirement

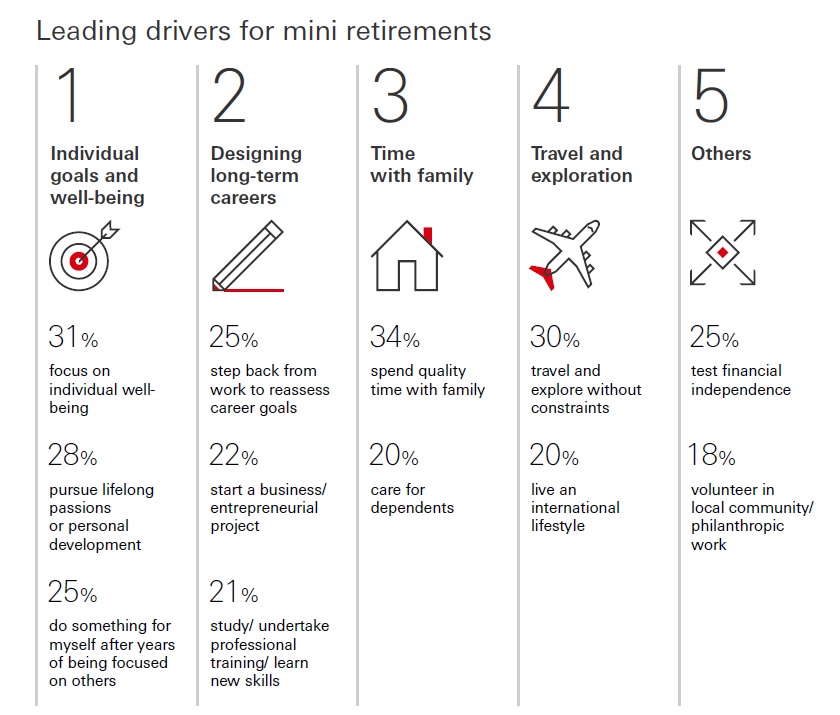

The leading drivers for mini retirement among respondents include pursuing individual goals and well-being, taking a step back from work to reassess career goals, spending quality time with family, travel and exploration, and other activities such as philanthropic work.

Ensuring financial security for your mini retirement and the long haul

The report finds a tension between short-term aspirations and long-term goals of respondents, with more than 30% of affluent investors indicating that they plan to draw from pension plans or retirement accounts to fund their mini retirements – and that they will need more savings for their final retirement.

An increasing number of affluent investors across all generations are also now placing greater importance on maintaining their pre-retirement standard of living in their final retirement. With the cost-of-living ranking as their top concern, it’s no surprise that the view among respondents in 2025 is that they will need up to 34% more savings to feel comfortable and secure in their final retirement, than last year (USD1.05m in 2025 versus USD780,000 in 2024).

Whatever your approach to retirement, financial security is an important consideration that requires an objective assessment of what savings you will require. It’s important to regularly review and assess your plans to ensure you stay prepared for changing personal circumstances and protect yourself against inflation.

Engaging a Wealth Specialist or Advisor is crucial as you can benefit from creating a personalised financial plan that empowers both short-term aspirations and long-term goals. It’s crucial to not solely rely on dividends and interest but also explore avenues for generating a steady income that can withstand the impact of inflation to empower you in planning a multi-retirement journey.

If you’re considering a non-linear retirement, think about these 5 steps:

- Assess your budget: Your current financial situation and cash flow are important when planning for any specific activities or experiences you want to pursue in your non-linear retirement such as travel, education, classes, or hobbies. It’s important to decide on how your absence from work will affect your retirement savings and pension entitlements. Consider adjusting on your pension contributions during your mini retirement if possible or estimate how your retirement plans will be impacted.

- Seek professional guidance: You might benefit from getting expert advice to create a financial plan to fulfil your mini retirement aspirations and a plan to support your expenses after you retire. Professional support can provide an objective assessment of the savings needed to achieve your desired lifestyle, including an emergency fund during mini retirement - it’s never too early to start investigating this.

- Explore the timing of your break and consider your career roadmap: The difference between a good decision and a bad one can be timing. Think about what would make sense for you based on your life stage, family circumstances and the opportunities you have in the next few years.

- Consider healthcare costs: Evaluate your health insurance options during your break, including whether your current plan covers you while you are away from work or if you need to acquire personal coverage for your mini retirement. Keep in mind any implications for your healthcare plan after you retire, should you take a mini retirement now.

- Identify extra income sources: Revisit existing or explore new income sources you could leverage during mini retirement to support you to grow your pension savings. Consider products and investment strategies which could increase your financial security and safeguard your savings from the impact of inflation over time, such as developing a diversified portfolio.

Financial goal planner

Be future ready with HSBC Wealth Management Services and start the journey by selecting your goals

Investment Plans

Investment options for a range of financial goals