8 December 2025

In a unanimous decision across the six MPC members on 5 December, the RBI cut the policy repo rate by 25bp, taking it to 5.25%. This was in line with our expectation. But this is not where the accommodative policy ended.

The RBI also unveiled its plans to infuse domestic liquidity, announcing INR1trnOMO purchases of government securities and a 3-year USD/INR buy-sell swap of USD5bn in December. These, we believe, can infuse about INR1.45trn of liquidity in December.

Dovish on many counts

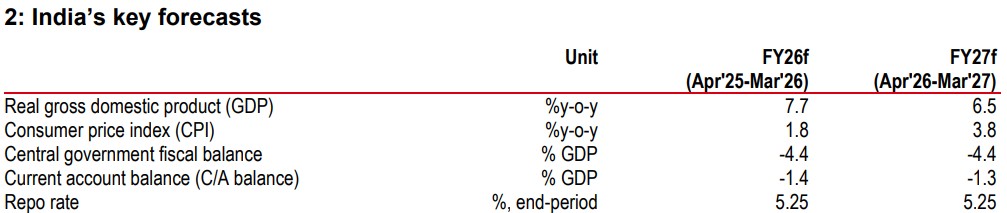

On inflation, the RBI lowered its FY26 and 1HFY27 inflation forecasts by 60bp and 50bp respectively. It further emphasised that underlying inflation (core excluding gold) is even lower (at 3% in the last 3 months).

On growth, GDP numbers were raised, from 6.8% to 7.3% in FY26, but in our view, primarily on the back of stronger-than-expected numbers in 2QFY26. The governor spoke about the exports sector being weaker in the press conference and he also said that he expects “growth to somewhat slow”.

On liquidity, not only is the RBI providing INR1.45trn worth of funds in December, the governor mentioned that more could be made available if needed.

On rates, the governor mentioned that in the season of easing, the odds for lower rates are more than for higher rates.

Why this dovishness?

We believe there are two main reasons for the dovishness this time.

First, the inflation targeting regime has some symmetry (4%, +/-2%), which needs to be respected for the regime to strengthen and succeed. We would expectrate hikesand hawkish commentary if inflation were to run higher than 6% for 6 months. In the same vein, if inflation runs lower than 2% for 6 months, we would expect the RBI tocut rates and sound dovish, which is what it did in the December policy meeting.

Second, the macro economy needs loose monetary policy as per our forecasts. We expect inflation to remain below 4% in FY26 and FY27. We believe growth is strong now, but will soften bythe March quarter due to fiscal tightening, weaker exports, and the GST boost fading. We think fiscal policy will remain tight in a world of fiscal intolerance, and the onus for supporting growth will fall on the RBI.

What next?

Even though the RBI has lowered 1HFY27 inflation forecast by 50bp (4.5% previously to 4% now), our forecasts are 50bp lower (c3.5%). If we are correct, and the RBI eventually makes further downward adjustment to inflation, there would be space to ease further, if growth requires it. As such, we believe there are risks of further rate cuts in FY27, alongside more liquidity infusion.

Finally, while the RBI did not provide much new colour on its INR policy, we believe the ongoing FX depreciation can be the best and most fitting shock absorber, improving export competitiveness in the face of elevated tariffs.

Additional disclosures

1. This report is dated as at 08 December 2025.

2. All market data included in this report are dated as at close 05 December 2025, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.