10 February 2026

Godot arrives. The wait for an India-US trade deal has been long. But it finally arrived on 2 February, though we are still awaiting details.

The US has agreed to lower the 50% tariff on India’s goods to 18%. This comes in two parts. One, President Trump announced that under a trade deal, India’s “reciprocal tariffs” will be set at 18% instead of 25%, effective immediately. Two, US officials said the extra 25% tariff related to Russian oil will also be removed, as India has reportedly agreed to stop buying Russian oil (Reuters, 2 February 2026). An official press release with details has not been released. There are three areas in which more clarity is needed:

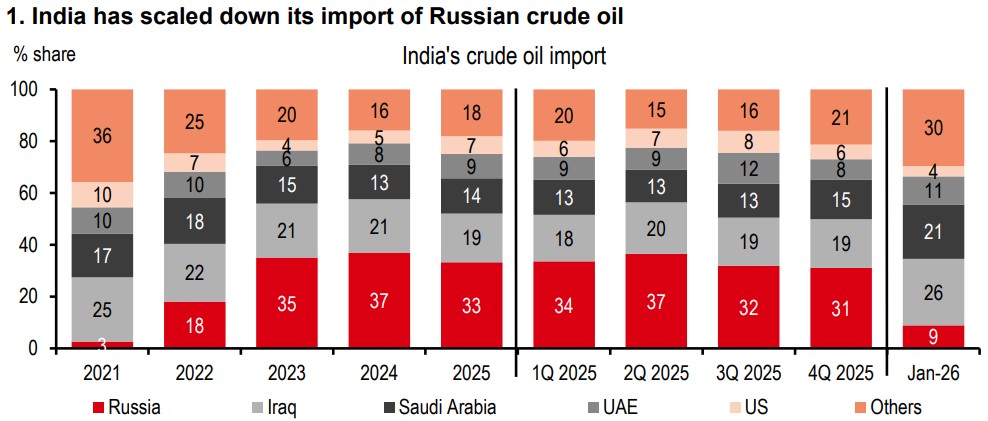

One, will India have to stop all Russian oil purchases? Import data shows India has already scaled down Russian purchases (Exhibit1). We also believe that the discount on Russian oil has fallen, so switching to other sources may not be too costly.

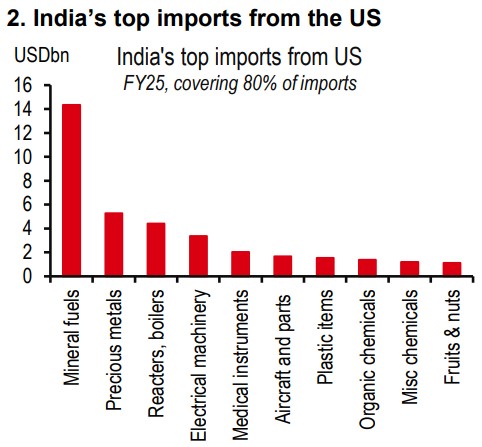

Two, what’s the timeline for the USD500bn of US goods (energy, technology, agriculture,and coal) that the US said India has agreed to buy? We believe India would switch suppliers rather than raise its overall import bill (Exhibit 2).

Three, the US President also mentioned that India will lower all tariff and non-tariff barriers on US goods to zero. The details are not out, but the India-EU trade deal could provide a framework under which both parties could safeguard some sectors.

Short-term growth impact. The US accounts for 20% of India’s goods exports (2.2% of GDP). In an earlier report we had calculated that the 50% tariff could shave off up to 0.7ppt from India’s GDP growth. With the tariff now more than halved, we believe the growth drag will halve to about 0.3ppt. These numbers assume that one-third of exports remain exempt from tariffs (e.g. pharmaceuticals, critical minerals, and fuels), and some sectors face differential tariffs (autos, steel, and aluminium).

The items that were most at risk were the labour-intensive jewellery, textile, and food items. These could get some reprieve (Exhibit 3). At the new 18% tariff rate, India has a rate marginally lower than the 19% levied on most ASEAN economies (excluding Singapore).

Medium-term growth impact.This is where we expect to see the most benefit. The US-India trade pact adds to a string of external reforms India has undertaken last year – completing FTAs with the EU and the UK, lowering some customs duties, and becoming more open to FDI. With these, India is putting exports centre stage as a key driver of growth, and benefitting from the China+1 theme.

Separately, it is also diversifying itsgrowth strategy as was clear from the just concluded Budget speech. From being focused on just high-tech goods and services exports, such as electronics and professional services, it is now also focusing on re-energising mid-tech exports, such as textiles. Given India’s wage advantage, this is a welcome strategy.

Lastly, external reforms are being complemented by domestic reforms, such as the ongoing government deregulation drive. Of course, much depends on implementation.

Inflation and BoP impact. There are several moving parts on inflation. Lower import tariffs and a more stable currency should lower inflation. However, switching to more expensive oil, and a change in the CPI base year could marginally raise inflation in FY27. The impact of none of these factors, we believe, will be large. And in most parts will offset each other.

The excess capacity from China driving disinflation remains strong. And we continue to believe that inflation will remain close to the 4% RBI target. All of this means that the central bank should be able to hold the repo rate steady for the foreseeable future, while focusing on providing enough liquidity.

Meanwhile, if the improvement in sentiment and push for exports raises capital inflows, the balance of payments deficit would fall, supporting the currency.

Additional disclosures

1. This report is dated as at 03 February 2026.

2. All market data included in this report are dated as at close 02 February 2026, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.