29 January 2026

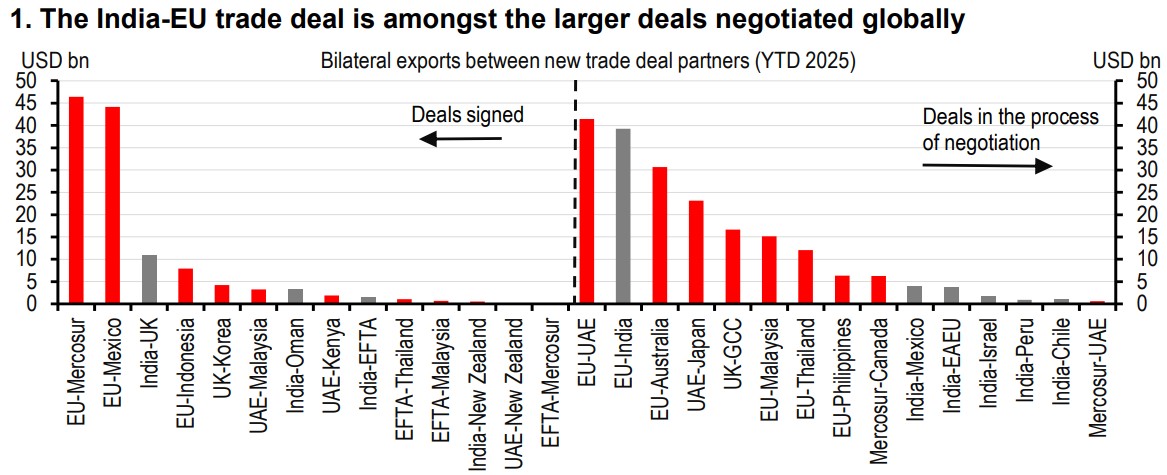

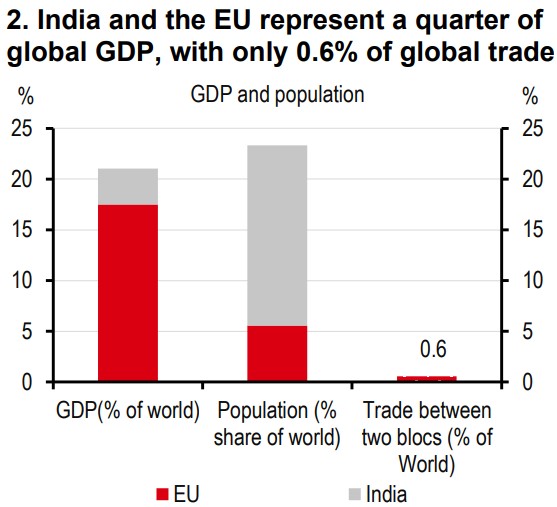

After a two-decade long negotiation, India and the EU have finally sealed a Free Trade Agreement (FTA). The implementation is likely in 2027, following legal vetting and EU parliamentary approval. This is amongst the larger global trade deals recently negotiated. India and the EU combined account for around 25% of global GDP, and the deal is billed as the largest ever made by both sides. The potential for growth is substantial, given the trade in this region is only 0.6% of global trade. The benefits could eventually go beyond goods trade, including larger FDI flows, more services trade, and strategic diversification.

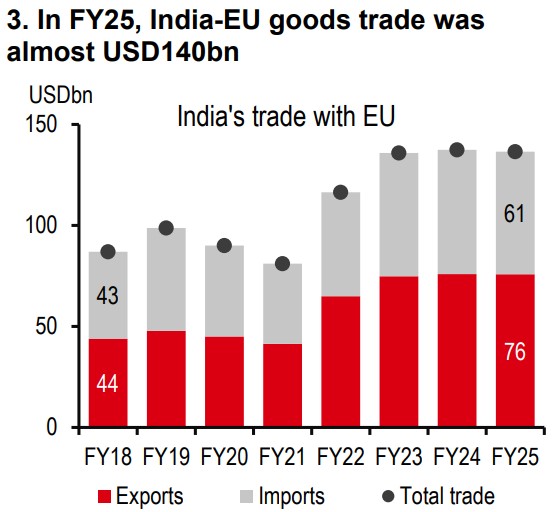

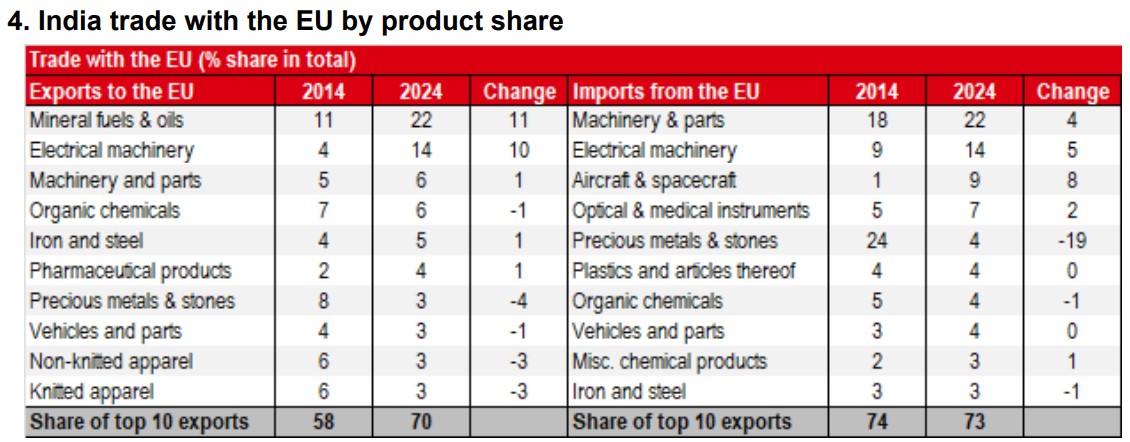

The FTA is described as the “mother of all deals” – which is balanced, yet ambitious and mutually beneficial for both parties.In FY25, India-EU goods trade was almost USD140bn. Details show that the India-EU trade is built on complementary value chains. The EU sells capital goods and industrial inputs to India (such as high-end machinery, electronic components, aircraft, and medical devices). India sells labour-intensive and consumer-focused goods to the EU (such as smartphones, garments, footwear, pharmaceuticals, auto parts, and diamonds, though fuel tops the list).

As per the press release, the trade agreement aims to liberalise 92-97% of tariff lines. Officials hope the deal will double bilateral trade within five years.

In detail, several sectors are to be liberalised, while respecting red lines on both sides:

Services trade is likely to benefit from preferential access (e.g. in financial services). Labour may benefit from easier mobility norms. Investment may get a boost from supply chain integration and deeper partnerships (for instance, in defence)

EU-India trade remains limited, with room to grow

Meaningful unrealised potential. As a block, the EU is India’s largest trading partner. In FY25, India exported USD76bn of goods to the EU and bought USD61bn of goods from the EU. Prior to this trade deal, the ITC export potential map showed that c50% of India’s export potential to the EU remains untapped. As per ITC, large gains are possible across several sectors – machinery, jewellery, electronics, pharmaceutical components, and textiles[@india-economics-05-01].

of India’s export potential to the EU remains unrealised

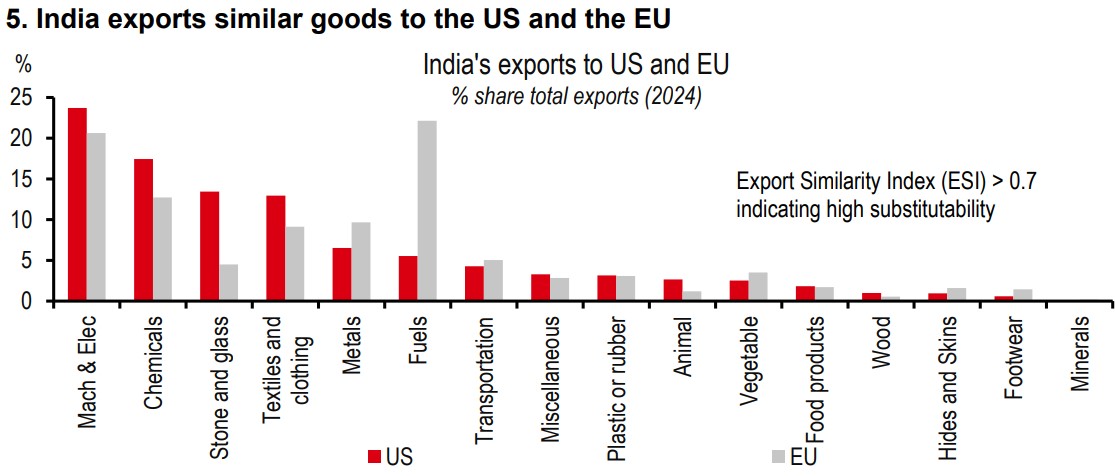

Substitute for US exports. The 50% tariff imposed by the US on India’s exports has led to efforts by Indian exporters to look for new destinations. Interestingly, India’s exports in value terms to the EU (USD76bn in FY25) and the US (USD87bn) are in the same broad range, and the products traded are also similar (see exhibit 5, barring the large fuel exports to the EU). From that perspective, the EU could be a region that India wants to focus on, to redirect some of its exports.

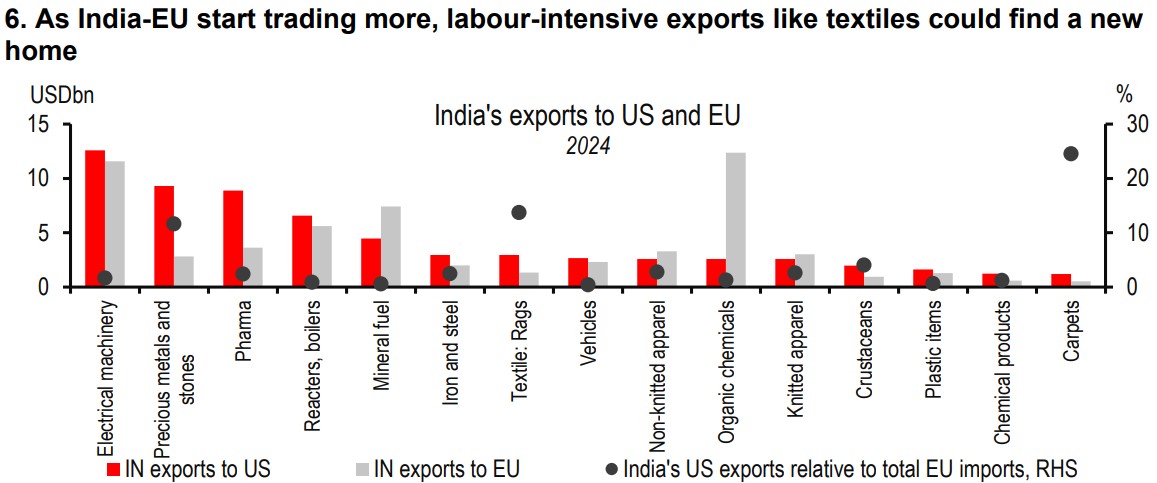

Indeed, labour intensive sectors, such as textiles and gems and jewellery, were most at risk with the US tariffs (see exhibit 6). These may now benefit from tariff elimination in the India-EU trade deal.

In the medium term, gains could be larger and beyond goods trade, spilling over into FDI flows (India currently gets 16% of its FDI from the EU), and more integration in services trade (c20% of India’s IT exports currently go to the EU).

External reforms strengthen. This trade deal follows other recent external sector reforms. India signed several trade deals last year, including deals with the EU, New Zealand, and Oman. It is opening up more sectors for FDI (e.g. FDI limits in insurance have been raised from 74% to 100%). And it is lowering tariffs on imported intermediate inputs (we expect more on this in the 1 Feb budget). As we have previously described,these steps should help grow India’s manufacturing sector, which has been a laggard, especially when compared with India’s services exports.

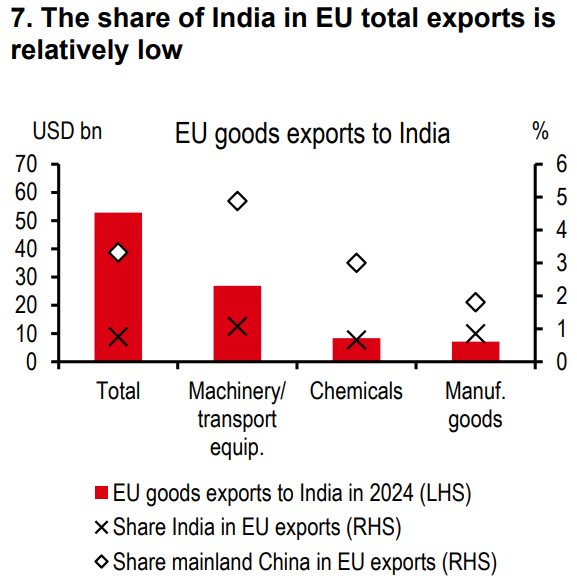

From the EU’s point of view, the deal also represents an opportunity to improve its access to a large market (1.4 billion people) that is still relatively closed. Today, India represents only 0.8% of the EU’s exports in goods, versus 3.6% for mainland China for example. Given the focus on cars in the deal, there is potential to increase the share of India in EU exports in machinery and transport equipment (1.1% versus 4.9% for mainland China), a sector that represents the largest part of EU exports to India (see Exhibit 7). There could also be an opportunity for the European defence industry, given the willingness to strengthen defence ties via the EU-India Security and Defence Partnership.

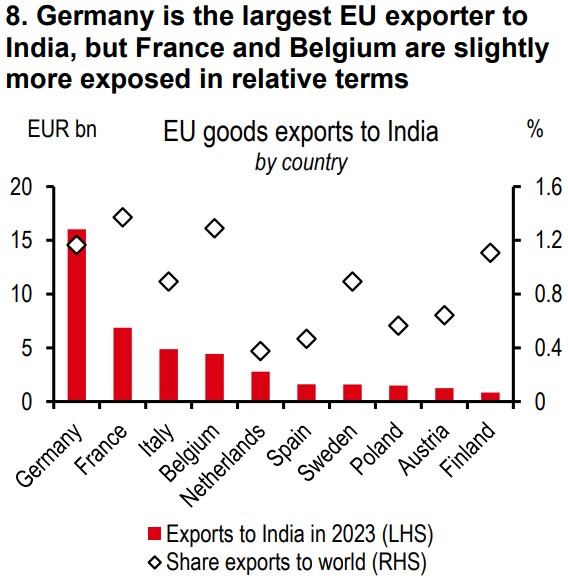

The trade deal could especially benefit Germany, France, and Italy as they are the EU countries that export the most to India in absolute terms (with respectively 35%, 15%, and 11% of EU exports to India, see Exhibit 8). In relative terms, India represents the higher share of total exports for France (1.4%), Belgium (1.3%), Germany (1.2%),and Finland (1.1%).

Beyond trade, the deal also has strategic implications for the EU as it allows to strengthen the diplomatic and defence ties with a key strategic partner in Asia. It also supports diversification away from China and the US, extending the push seen with the recent EU-Mercosur deal.

Risks: That said, EU farmers may protest against agricultural imports from India. The FTA still needs to be approved by the European Parliament (EP), which would take at least a year. Recently, the European Court did not approve the EU-Mercosur deal, which now awaits judgement by the EP.

Secondly, the EU’s carbon border levy could blunt some tariff gains for India, especially for sectors such as steel, although today’s press release mentions some flexibility has been secured. Either way, key sectors like pharma and textiles are relatively less carbon intensive.

Additional disclosures

1. This report is dated as at 28 January 2026.

2. All market data included in this report are dated as at close 27 January 2026, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.