19 November 2025

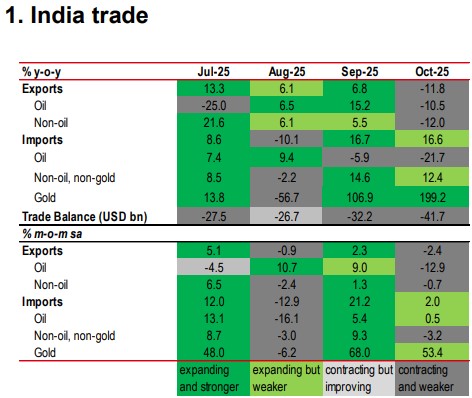

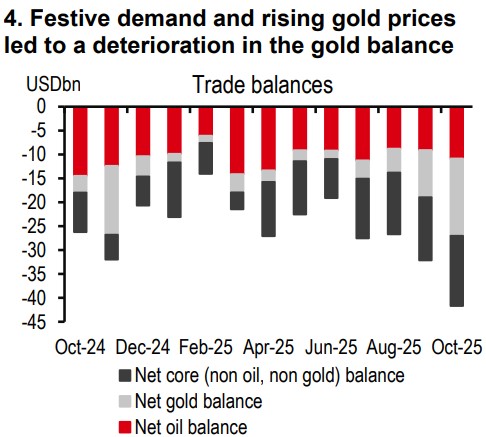

India’s goods trade deficit widened in October to USD41.7bn, an all-time high, from USD32.2bn in September. Seasonal trends indicate that the trade deficit tends to widen in October due to festive demand. After seasonally adjusting, the trade deficit stood at USD33.4bn (vs USD31.1bn in September). In detail, while both rising imports and weaker exports played a role, the former dominated.

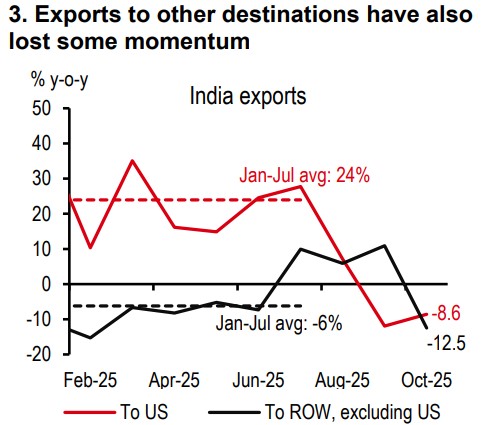

Export drag continues. Exports to the US contracted in y-o-y terms for a second consecutive month (-12% in September, and -8.6% in October). The granular breakdown will be released in a few days; however, we can get a glimpse of the tariff drag in overall export numbers. Export of gems and jewellery, leather, and chemicals contracted (in line with the trends observed in September). However, exports of exempt categories like electronics continued to rise.

Exports to non-US destinations lost momentum. After rising 11% y-o-y in September, it slipped back into the red, in line with the trends observed in 1H25. Some of this could reflect the heightened competition of selling to non-US destinations as many countries try to diversify exports post tariff announcements. Another could be that India is not as well integrated into global supply chains and large aggregators, which assist in rerouting and tariff optimisation.

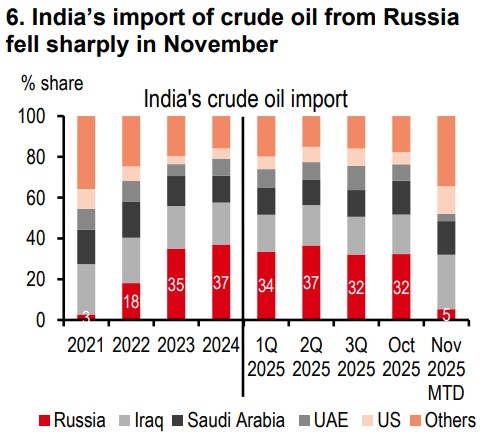

Gold imports sting. Gold prices were up 58% y-o-y in October, the Diwali month. No surprise, the gold import bill rose to USD14.7bn (USD5bn higher than in September). Core imports (non-oil, non-gold) contracted on a sequential basis following a sharp rise last month, select categories like electronics, machinery, and machine tools grew quickly. Electronic imports, in particular, may have risen on the back of GST rate cuts.

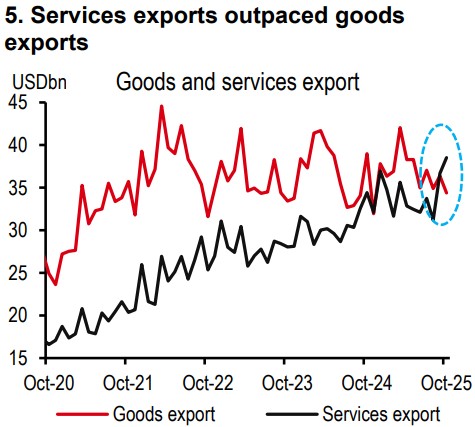

India’s services exports (USD38.5bn) outpaced goods exports (USD34.4bn) in October. After a few months of weakness, services exports bounced back (averaging cUSD37.5bn in September-October vs USD33bn in the first eight months of the year). Services trade surplus was at an all-time high of cUSD20bn.

Current account deficit for 4Q25 is likely to settle close to 2.7% of GDP given the USD42bn deficit in October and assuming cUSD29bn goods deficit for November-December (a scenario where demand for precious metals fades). If the trade balance continues to average cUSD29bn in 1Q26 as well, then the full-year current account deficit may more than double to 1.4% of GDP (vs 0.6% in FY25).

A potential trade deal with the US in the next few months could help offset the current drag on exports and thereby, growth. This comes at a time when a trade deal with the UK has already been struck and one with the EU is in advanced discussion. Eventually, India may also want to look east, and get further integrated into supply chains, if it wants to grow as an exporter. Meanwhile, the 10%-odd depreciation in the real trade weighted exchange rate this year, could help improve export competitiveness.

Additional disclosures

1. This report is dated as at 18 November 2025.

2. All market data included in this report are dated as at close 17 November 2025, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.