14 Oct 2025

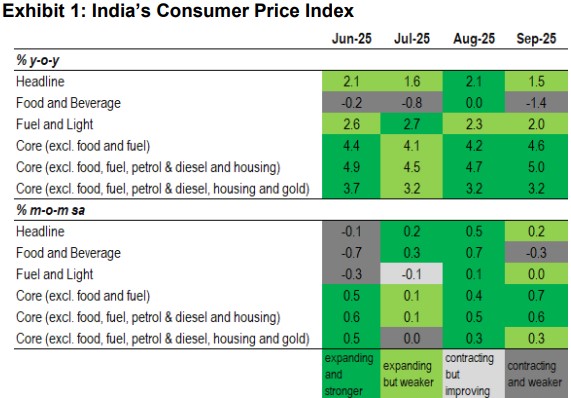

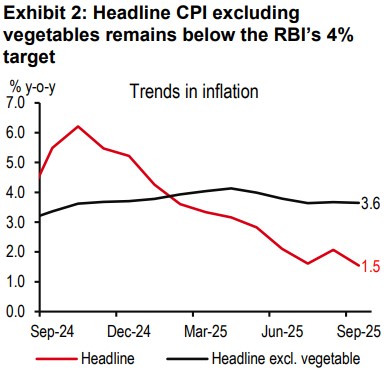

September CPI inflation came in at 1.5% y-o-y, the lowest since June 2017, in line with market expectations. Sequential momentum slowed to 0.2% m-o-m sa (vs 0.5% last month). Excluding vegetables, headline inflation came in at 3.6% y-o-y (vs 3.7% previously). Average inflation for 3Q came in at 1.7%, slightly below the RBI’s forecast of 1.8%.

Food prices slipped into the red on an annual basis. In sequential terms, too, food prices deflated 0.3% m-o-m sa (vs +0.7% in August). Recall, excessive rains in August had caused a sharp rise in vegetable prices. This appears to have reversed as vegetable prices are back in deflation. Apart from that, heavyweight cereals (weight: 9.7%) and pulses, alsoremained in sequential contraction.

Gold prices keep core inflation high. Recall, gold has a weight of 1.1% in the CPI basket, and was up 47% y-o-y in September. It alone contributed c50bp of the rise in headline CPI. Our preferred definition of core (excluding food, energy, housing,and gold) has been steady at 3.2% y-o-y in 3Q25. Sequential momentum, too, remains under the long-term average. That being said, the uptick in personal care items (excluding gold) is worth noting (+0.7% m-o-m sa). Hopefully, a pick up in the pass-through of GST rate cuts will soften its momentum.

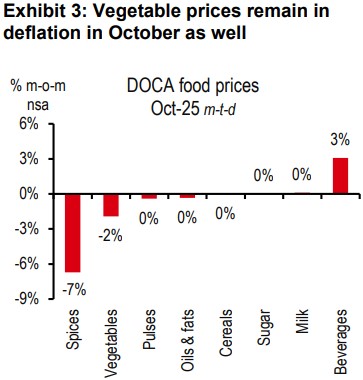

October’s inflation print is trending below 1%, even lower than September’s low reading of 1.5%. Vegetable prices during the first 10 days of October have eased in the range of 3-5%.

Strong cereal production and well stocked granaries are likely to help keep a lid on food inflation over the near term. And it is not just easing food prices, the high base of last year is likely to keep CPI inflation soft over the next few months. Global oil prices have been low, too, notwithstanding the volatility. Weaker growth, and cheaper exports from China arelikely to ensure inflation remains soft. To sum it all up, we are not too concernedabout the underlying inflation momentum.

Growth may see renewed weakness.The PMI index for September showed a fall in new export orders,which was being offset by new domestic orders. But this could change post Diwali when domestic orders slow. Government spending, particularly capex, which has been growing 43%y-o-y y-t-d (April-August) may also begin to slow in 2HFY26 to settle close to the budgeted growth of 10%. The single deflator boost, too, may begin to fade by the end of the year. We believe that if the 50% tariff sticks until the end of the year, the RBI will cut rates by 25bp in December, taking the repo rate to 5.25%. And we may also see a fiscal package for exporters around then, along with more economic reforms.

Additional disclosures

1. This report is dated as at 14 October 2025.

2. All market data included in this report are dated as at close 13 October 2025, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.