24 March 2026

Why does the oil price shock feel different this time? Varying prices of different oil price benchmarks are creating some uncertainty, but we believe it is natural gas and LPG unavailability that are at the heart of concerns in India, given high reliance on Middle Eastern supplies, low strategic reserves, and the recent doubling of cooking gas connections, bringing the shock closer to home. We calculate a 25% supply shortfall in natural gas, which could shave off 25bp from annual GDP growth if it lasts a full quarter.

Is it more a growth or a price shock? Currently the majority of the oil price burden is being borne by the public sector, i.e. the oil Public Sector Undertakings (PSUs). For now, it is more a growth shock than a price shock, since most pump prices are supressed. But if the oil shock lingers, and pump prices are raised (say after April state elections), the private sector would partake more evenly in burden-sharing, though inflation could rise.

Will consumers or corporates suffer more? Corporates tend to split the cost of higher oil prices between lower profits and higher consumer prices in a 40:60 ratio. Consumers bear a double sting –higher pump prices and higher non-oil prices passed on by corporates. The overall burden sharing ratio between corporates and consumers is 30:70.

Which variables are coming from a position of strength? In descending order, we outline four. Oil PSU margins were high and are able to withstand losses for now. Inflation was low and can withstand a moderate oil and weather shock, provided no changes are made in the inflation targeting framework which is undergoing review. Growth has been strong, though led by low commodity prices and normal rains, which are reversing. Alas, the BoP has been in deficit for a while. Some FX adequacy metrics need monitoring.

How will various economic variables fare? We outline sensitivities to various oil prices. The external balance will take an immediate hit. Then comes the growth hit, higher if the public sector is bearing much of the burden. Inflation is set to rise, but could remain below the 6% cap. Finally, allowing pump prices to rise will keep a lid on the fiscal deficit.

What can the RBI do? We believe the 8 April meeting will be all about communication to address the anxiety around the oil price shock. We expect the RBI to outline scenarios, sensitivities, and broad tenets of their reaction function. Despite the oil price shock we don’t expect rate hikes over the foreseeable future as we believe the RBI will focus on one-year ahead inflation, which may look softer than inflation in the immediate months.

It’s been 23 days of conflict in the Middle East and disruption in energy markets. While broad sensitivities of economic variables to the oil price are well known (for instance, as per the RBI, a 10% rise in oil prices lowers growth by 15bp, and raises inflation by 30bp), they tend to be calculated from long-term data across previous episodes, and each episode may have differences.

We ask what’s different this time, and where could we see a differentiated impact on the economy. We consider ‘starting points’ of various variables, ‘burden sharing’ across stakeholders, ‘longevity’ of the oil shock, and ‘substitutability’ across energy sources, to answer some pressing questions on economic impact and market reaction.

Oil price shocks have always hurt the economy, and are likely to do this time too, but sentiment seems to have taken a bigger hit this time. What’s different?

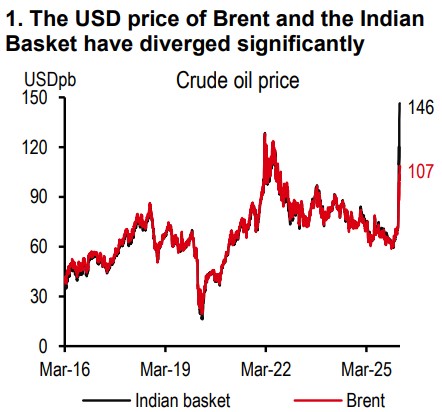

Various prices are moving differently for crude oil. The USD price of Brent and the Indian Basket, which earlier moved in line, have diverged significantly, with the former at USD107/bbl, while the latter is at USD146/bbl (as of 20 March, see exhibit 1). This may not be a prime concern for now, as the Indian Basket price has been pushed up by the Oman and Dubai crude components, where the supply is constrained and free-float is limited. As such the price reflected is not what India is paying for oil currently. But it is still a reflection of physical dislocation in the region, leaving a concern that once temporary global buffers are used up, prices of other oil benchmarks could rise.

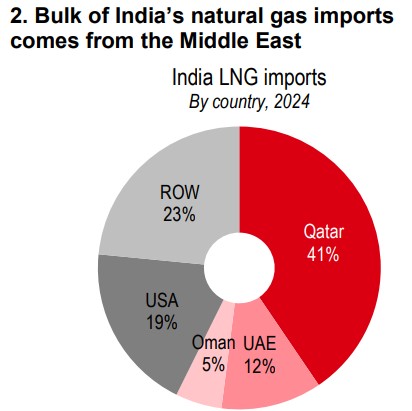

But the worries do not end there. We believe the LPG and natural gas availability uncertainty is creating panic. India imports 60% of its LPG needs. Of this, 80% of comes from the Middle East, most of it passing through the Strait of Hormuz. Of the 50% natural gas that India imports, Qatar, where supply has been disrupted, supplies the most (see exhibit 2). The global spot market alternative has seen prices more than double (in fact more than the rise in oil prices). Also worth noting is that a lack of underground storage facility in the case of gas means that strategic reserves are low and even short-term disruption in global supplies hurts.

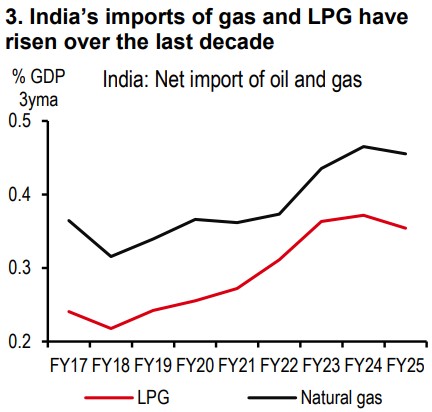

All of this matters more now because reliance on gas has only risen in recent years. In a way, India has become a victim of its own success. It tried to shift gently from coal to a greener alternative, gas, for industrial use, and from coal to LPG for household use[@india-economics-01-01]. India’s imports of natural gas and LPG have risen over the last decade (see exhibit 3).

As such, even though the overall usage of gas is lower than that of crude oil, lack of availability is now closer to home, denting sentiment.

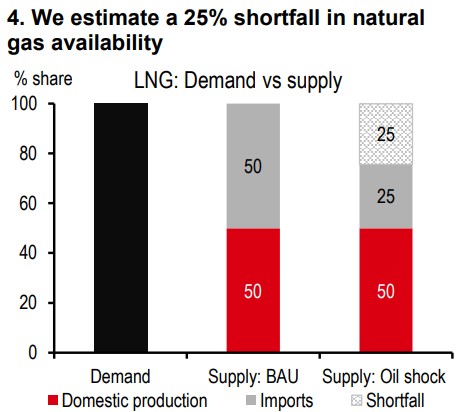

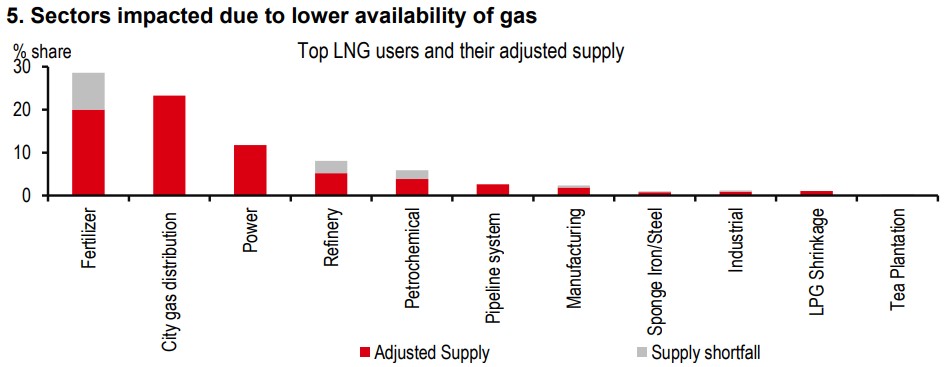

We estimate that at the current levels of production, consumption and imports, there could be a shortfall of 25% in gas availability (see exhibit 4)[@india-economics-01-02]. The government has responded by setting quotas for the industrial/commercial use of gas and LPG. Exhibit 5 outlines the big users of gas and the quotas they are allocated.

We map each of these to their direct share in GDP. Assuming that 50% of gas users can substitute with other sources of energy, the 25% gas shortfall could shave off 25bp directly from GDP growth if it lasts for a full quarter.

Bottomline – Varying prices of different oil price benchmarks are creating some uncertainty, but we believe it is natural gas and LPG unavailability that are at the heart of concerns in India, given high reliance on Middle Eastern supplies, low strategic reserves, and the recent doubling of cooking gas connections, bringing the shock closer to home. We calculate a 25% supply shortfall in natural gas, which could shave off 25bp from annual GDP growth if it lasts a full quarter.

An oil price shock is a classic supply shock lowering growth and pushing up inflation. Burden-sharing ratios determine which variablehurtsmoreon the margin.

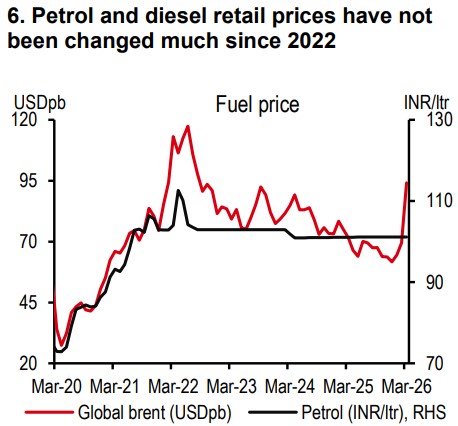

So far, pump prices of petrol and diesel have not been changed (barring a INR2.35 per litre increase in the price of ‘premium’ petrol rates, not ‘regular’ petrol, see exhibit 6).For crude oil, the burden is mostly falling on the public sector. For gas it is an even mix given half of the industrial users are public companies, and half private companies. Overall, the public sector is picking up the majority of the burden.

This has been made possible because of favourable starting points. Oil PSUs were making good profits before the oil shock, so they can withstand a loss for some time. The loss will be faced by the government too, in the form of lower dividends. While this goes on, the growth shock will be higher than the price shock, simply because pump prices are being suppressed.

But if the oil price shock lingers, oil PSUs may not be able to take all the burden and pump prices may be raised. Consumer (and corporate) purchasing power will take some of the hit, but it is worth noting that consumers don’t fully cut spending when faced with a shock. They can also draw down savings. In fact, their marginal propensity to (or not to) consume is generally around 0.7, rarely 1.

This behaviour can differ from the government’s, which has fiscal targets and may cut spending elsewhere to bear the oil burden. In short, as the burden starts getting shared by the private sector, the growth shock may ease at the margin. And the price shock may rise.

What does it mean for the RBI? As long as pump prices remain unchanged, the central bank can remain more focused on growth, as it currently is, with strong domestic liquidity support. But if the expectation is that pump prices will be raised over time, it cannot avoid the inflation angle.

Bottom line: Currently the majority of the oil price burden is being borne by the public sector, i.e. the oil PSUs. For now, it is more a growth shock than a price shock, since most pump prices are supressed. But if the oil shock lingers, and pump prices are raised (say after April state elections), the private sector would partake more evenly in burden-sharing, though the price shock could rise.

If high oil prices stick for longer, the subsidy bill for the government will rise. It may be a good idea to raise pump prices then, not just for fiscal sustainability, but also other macroeconomic adjustments (e.g. higher pump prices will incentivize lower demand from consumers, lowering oil imports). Once pump prices are raised, consumers and corporates will share a bigger burden than they are bearing now. Who will suffer more?

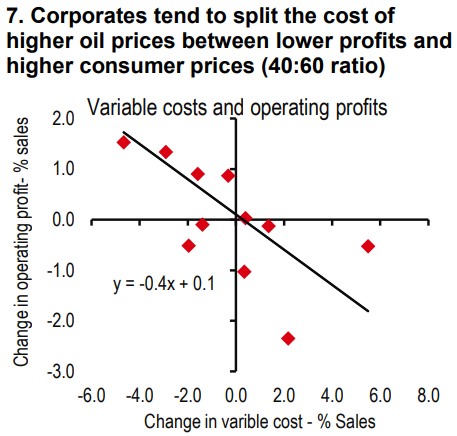

Let’s start with corporates. The pain to corporates from higher oil prices can either be absorbed in the form of lower profits, or can be passed on to consumers as higher prices, or a combination of both. Our analysis suggests that for every 1ppt rise in input costs, profits tend to fall by 0.4ppt (see exhibit 7), and the remaining 0.6ppt tends to be passed on to consumers as higher prices. From this perspective, the burden sharing between corporates and consumers is 40:60.

But this is not all that the consumers bear. They grapple with a higher price of petrol and diesel they buy (mostly for transportation), as well as face higher prices for non-oil products which corporates pass on to them.

Once we add up across all the channels, we find that the burden-sharing ratio between corporates and consumers is 30:70. This may put a floor on corporate profitability in the short run, but weaker demand would start hurting earnings over time.

Bottom line: Corporates tend to split the cost of higher oil prices between lower profits and higher consumer prices in a 40:60 ratio. Consumers bear a double sting –higher pump prices and higher non-oil prices passed on by corporates. The overall burden sharing ratio between corporates and consumers is 30:70.

Starting points matter. Variables which are coming from a position of strength can withstand the pressure of higher oil prices better and for longer. Here are a few that are worth looking into in descending order:

Oil PSU margins – as discussed earlier, because oil PSUs were making good margins in the run up to the oil shock, they can absorb losses for some time, keeping pump prices and inflation under control.

Inflation – Good food production and imported disinflation from China kept CPI inflation at low levels in FY26. Even a 0.5-1.5ppt rise led by the oil shock would still keep inflation within the flexible inflation targeting band of 2-6%. As long as these are short term supply shocks of no more than a year, the RBI may not feel pressured to raise rates for now.

What is importantthough is that no significant change is made to the Inflation Targeting framework, which is undergoing its periodic review. Now is the time to focus on macro stability and predictability, at least in policy choices.

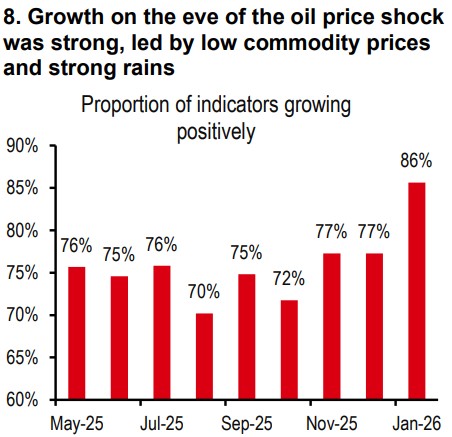

Growth – We find that 86% of the 100 indicators of growth we track were growing at a positive clip in January, making it a strong starting point (see exhibit 8). Having said that, some of this was led by positive supply shocks in 2025 –low oil prices and strong rains. Both may not be favourable in 2026 (the chances of an El Niño lowering rains has risen to 62%).

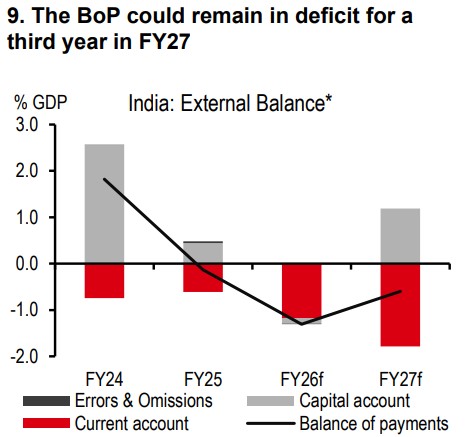

Balance of Payments. External accounts were not as strong before the oil shock. Led by capital outflows, the BoP was in a small negative for two years. And if oil averages USD80/bbl or more in 2026, the BoP could remain in deficit for a third year (see exhibit 9).

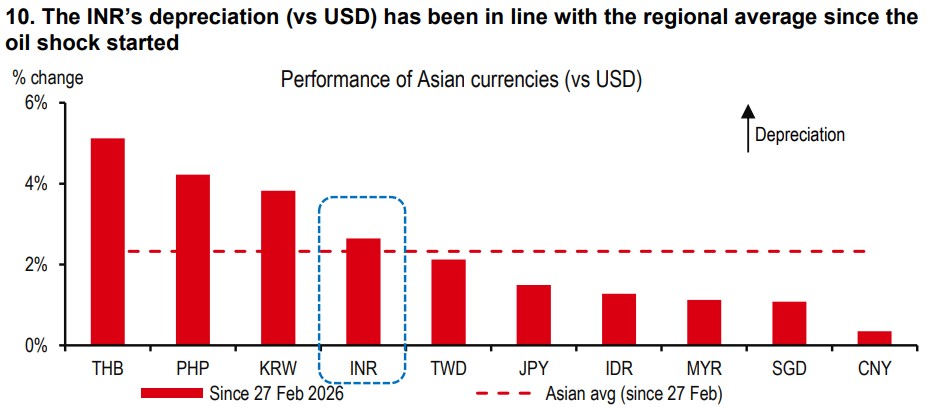

Market intervention has been high through March with FX reserves falling by USD19bn in a fortnight (27 February to 13 March), taking FX reserves to USD710bn. The INR’s depreciation against the USD has been in line with the regional average since the oil shock started (see exhibit 10, though it has underperformed the region over a one-year horizon).

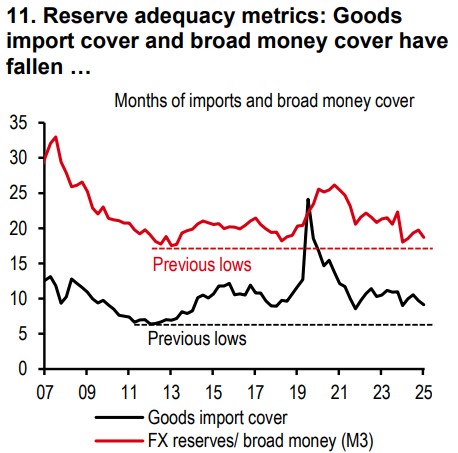

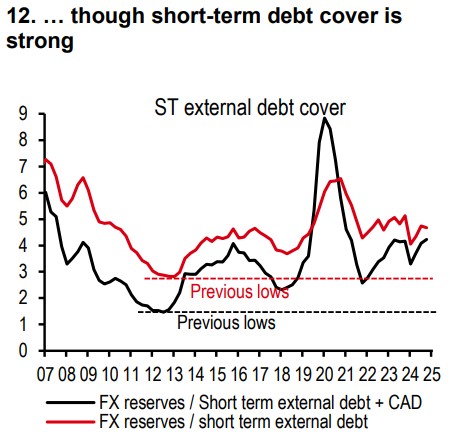

In net terms, FX reserves are even lower given the RBI’s rising short-forward book. The RBI may need to keep an eye on net FX adequacy. And here too, a range of metrics will help, which look not only at trade, but also capital flows and debt obligations. We find months of goods import cover and broad money cover approaching 2013 levels (when India was last under BoP stress), though short-term debt cover looks stronger (see exhibits 11 and 12).

Bottom line: In descending order, we outline four. Oil PSU margins were high and are able to withstand losses for now. Inflation was low and can withstand a moderate oil and weather shock, provided no changes are made in the inflation targeting framework which is undergoing review. Growth has been strong, though led by low commodity pricesand normal rains, which are reversing. Alas, the BoP has been in deficit for a while. Some FX adequacy metrics need monitoring.

Having outlined starting points, we discuss pressure points and outline sensitivities for key variables under different oil assumptions for the year (see exhibit 13):

Current account deficit – We expect a 10% rise in oil prices to push up the current account deficit by 0.3% of GDP. Capital inflows could also remain challenged in a risk-off setting. This is likely to keep the BoP in another year of deficit.

Growth – The main drivers of growth in the previous year are reversing. Both an oil and a weather shock could impact numbers in 2026. It has started off more as a growth shock than a price one with the public sector taking a bigger hit than the private sector.

Inflation – The weight of energy in the CPI basket has been raised, but primarily led by administered energy prices. As long as pump prices are kept unchanged, the rise in inflation will likely be rangebound. Wedon’t see average annual inflation crossing the 6% RBI’s upper limit.

Fiscal deficit – There will be pressure from lower taxes and higher oil and fertiliser subsidies, but offsets from higher RBI dividend, more inflows into the national small saving fund, and lower-than-budgeted capex. The slippage could remain rangebound if the government eventually raises pump prices (which we expect post the April state elections).

Bottom line: We outline sensitivities to various oil prices. The external balance will take an immediate hit. Then comes the growth hit, higher if the public sector is bearing much of the burden. Inflation is set to rise, but could remain below the 6% cap. Finally, allowing pump prices to rise will keep a lid on the fiscal deficit.

The 8 April policy meeting won’t be about what action the RBI takes. We don’t think there are expectations of rates change or other major measures from this policy meeting. But what this meeting will be critical for is communication to address some of the anxiety of the oil price shock.

We believe the RBI can bring in some domestic certainty by outlining various scenarios and sensitivities for oil prices, outlining impact on growth and inflation in each. This would help the public get a framework to think about various outcomes. It would also give confidence that the RBI has thought of all possibilities.

We expect no rate cutsor hikes in the current cycle, leaving the repo rate at 5.25%. We believe the RBI focuses on 1-year ahead inflation, which may look softer than the upcoming months, provided the oil price shock settles by the year-end.

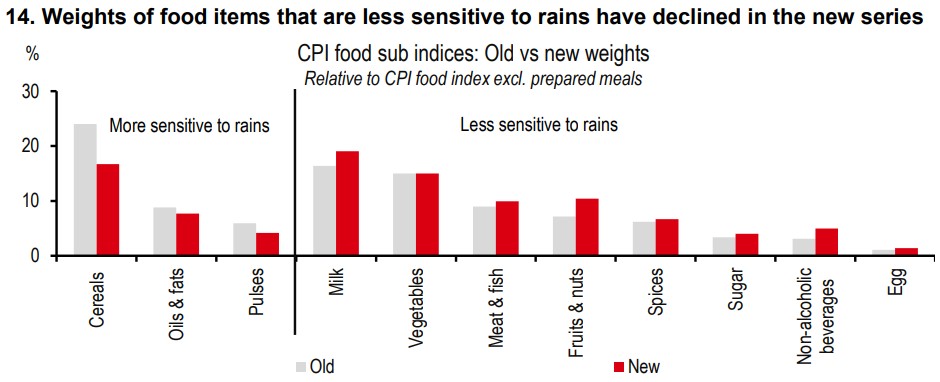

There are worries about the El Niño phenomenon taking shape in 2026 and stoking food inflation. We think the new CPI series may help withstand the El Niño inflation shock better. The overall weight of food has been lowered (from 45.9% to 36.8%). And moreover, the items where weights have been increased (like eggs, meat and fish) are less sensitive to rains, while items where weights have been lowered (like cereals) are more sensitive to rains (see exhibit 14).

Bottom line: We believe 8 April meeting will be all about communication to address the anxiety around the oil price shock. We expect the RBI to outline scenarios, sensitivities, and broad tenets of their reaction function. We expect no rate cuts nor rate hikes inthis cycle as we believe the RBI focuses on 1-year ahead inflation, which may look softer than inflation in the upcoming months.

Additional disclosures

1. This report is dated as at 23 March 2026.

2. All market data included in this report are dated as at close 19 March 2026, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, HSBC Private Bank Suisse SA, South Africa Representative Office, HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. Incorporated in Hong Kong SAR with limited liability. HSBC India is an AMFI-registered Mutual Fund Distributor of select mutual funds and a referrer of other 3rd party investment products. HSBC India does not distribute or refer investment products to those persons who are either the citizens or residents of United States of America (USA), Canada or any other jurisdiction where such distribution or referral would be contrary to law or regulation.

HSBC India will receive commission from HSBC Asset Management (India) Private Limited, in its capacity as a AMFI registered mutual fund distributor of HSBC Mutual Fund. The Sponsor of HSBC Mutual Fund is HSBC Securities and Capital Markets (India) Private Limited (HSCI), a member of the HSBC Group. Please note that HSBC India and the Sponsor being part of the HSBC Group, may give rise to real, perceived, or potential conflicts of interest. HSBC India has a policy in place to identify, prevent and manage such conflict of interest For more information related to investments in the securities market, please visit the SEBI Investor Website: https://investor.sebi.gov.in/ and the SEBI Saa₹thi Mobile App. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Issued by The Hongkong and Shanghai Banking Corporation Limited, India. Incorporated in Hong Kong SAR with limited liability. HSBC Bank ARN - 0022 with validity from 19-Feb-2024 to 18-Feb-2027. Date of initial registration: 19-Feb-2002.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

© Copyright 2026. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks.

In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.