27 Jun 2025

Positive developments

As we still await certainty around global tariffs and trade flows, three positive developments have taken place on India’s growth front recently.

One, inflation has fallen quickly, and this has raised purchasing power of the informal sector consumers across rural and urban India, who make up two-thirds of the consumption pie. This comes at a time rural production and incomes have risen and is likely to provide a much needed shot in the arm to consumption.

Two, the new leadership at the Reserve Bank of India (RBI)is easing policy quickly. Their steps include rate easing, liquidity infusion, and regulatory easing. Efforts to front-load much of the easing is likely to hasten transmission into deposit and lending rates, augmenting the supply of credit, even if the demand for credit, admittedly, will take longer to rise.

Three, services exports, which now make up half of overall exports, remain resilient. As we have documented in the past, they have moved up the value chain, from simple IT services exports to a host of professional services exports.

Resilient growth

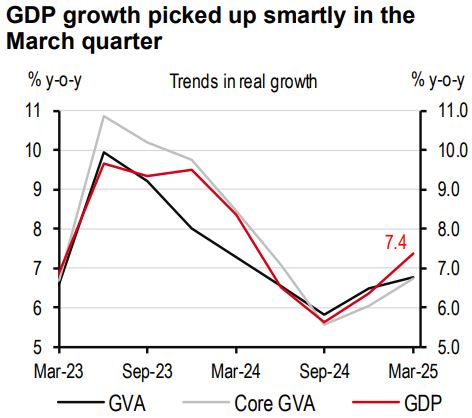

1Q25 GDP growth came in at 7.4%, stronger than 6.4% a quarter ago. The practice of cash accounting instead of accrual accounting in the subsidy bill may have inflated GDP numbers in the quarter; however, even the alternate growth measure, Gross Value Added (GVA), suggests a rise in activity in the quarter (6.8% versus 6.5% in the previous quarter). All said, we recently raised our GDP forecast from 5.9% to 6.3% for FY26 (6.2% to 6.7% for CY25).

We believe that within this headline improvement, some important changes will happen across sectors. Investment may come in weaker than before, and even weaker than consumption growth. Private capital expenditure generally weakens during periods of uncertainty. Consumption growth could come in stronger than before as informal sector consumption rises, even though formal sector consumption, which makes up the remaining third of the consumption pie, softens (led by uncertain equity market returns and global trade flows).

Can current global uncertainties be turned into opportunities over the medium term? We find that India has grown faster in periods of strong integration with the world. We further find that global financial integration has been strong, but global trade integration has been weaker. However, with the economy slashing import tariffs and fast-tracking trade deals, it may stand to gain once the tariff storm settles. As supply chains get rejigged once again, India could attract a larger share of manufacturing and exports, particularly in labour-intensive mid-tech goods like textiles.

Policy issues

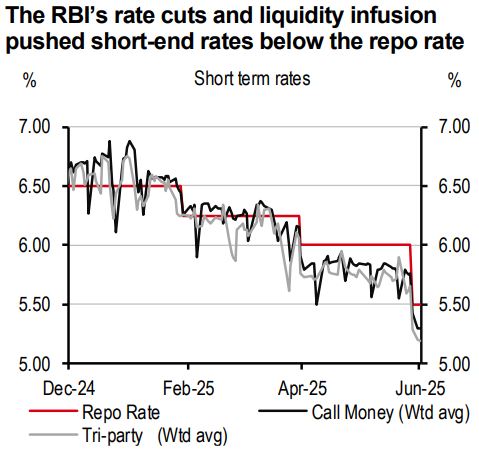

The RBI eased more than expected in the 6 June Monetary Policy Committee (MPC) meeting. One, it cut by 50bp, more than consensus expectation of 25bp, taking the repo rate to 5.50%, and delivered a 100bp in rate cuts in 2025 so far. Two, it cut the cash reserve ratio(CRR)by 100bp, a move that was largely unexpected. This cut is expected to add INR2.5trn to liquidity but could eventually be used to sterilise the USD40-45bn of FX swaps that are expected to mature between June and December. We see the repo rate and CRR cuts as a package to add liquidity, but in a way that supports banking sector net interest margins. Three, the stance was changed from accommodative to neutral. While the governor reiterated that after the RBI’s actions on 6 June, there is “very limited space” for further easing, we continue to expect a 25bp rate cut in the December quarter. The RBI forecasted inflation at 3.7% for FY26, but we believe it could come in lower at 3.2%, opening space for further easing.

It can be asked why the RBI eased so much at a time when growth is holding up. Our sense is that the RBI is using this opportunity to raise structural credit growth and potential GDP growth. In fact, the governor said that “while price stability remains the focus of monetary policy, we are not oblivious to putting in place complementary monetary and credit policies and regulations that support growth and prosperity”. This, to us, signals a new RBI. One that is not just focused on the current business cycle but also on India’s potential growth.

On the fiscal front, the government may choose to appropriate a part of the fall in global oil prices in the form of higher revenues instead of cutting pump prices. This could make fiscal consolidation much easier than budgeted. We think the fiscal deficit target of the government will be met, supporting India’s macro stability credentials. On the external front, the current account deficit is likely to remain low as long as investment remains soft. The area to watch, instead, are capital inflows. Net FDI inflows have been weak (because of large repatriation), and portfolio inflows remain unpredictable.

Additional disclosures

1. This report is dated as at 27 June 2025.

2. All market data included in this report are dated as at close 26 June 2025, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses toensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of afinancial instrument or of an investment fund.